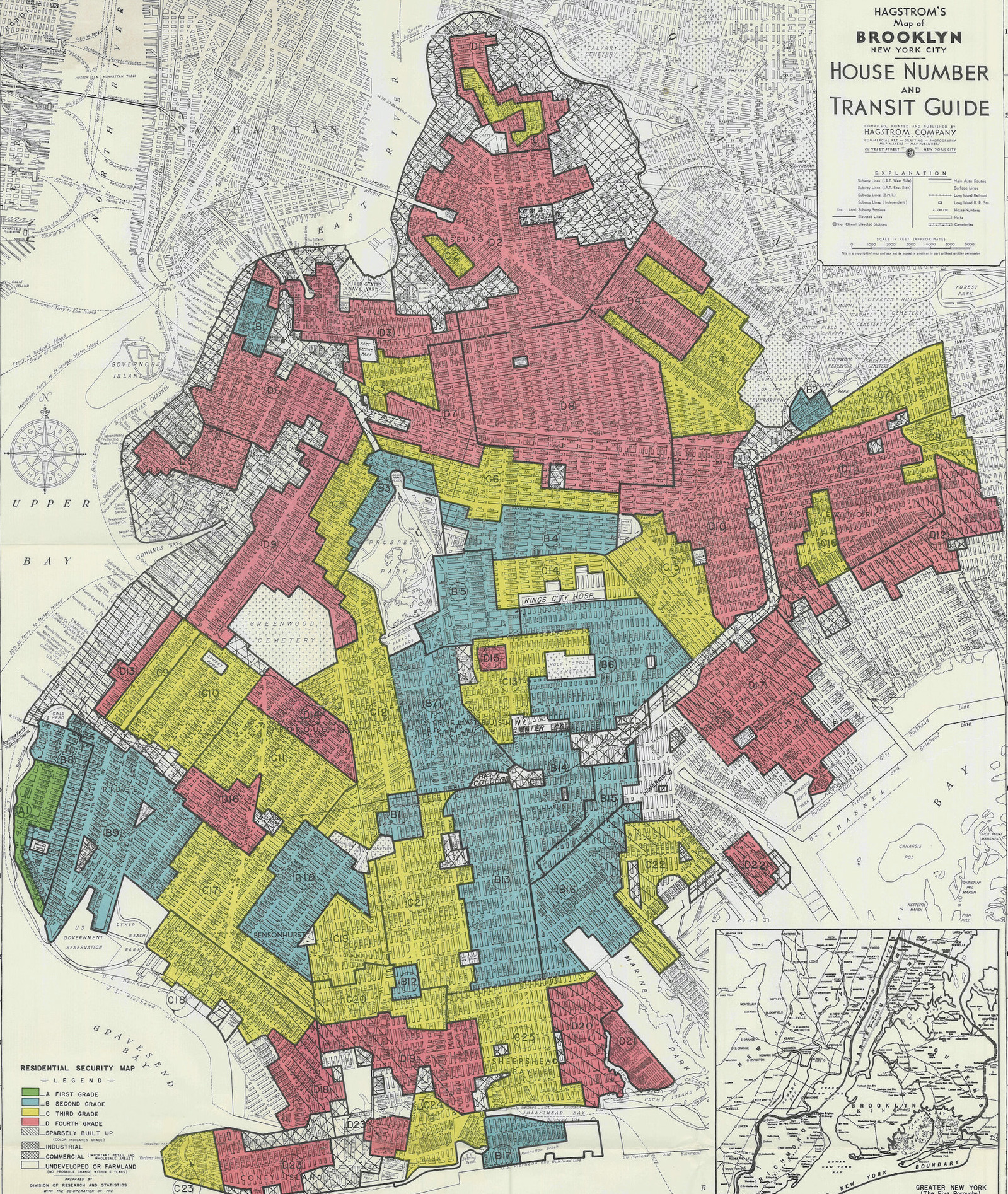

Green: New, desirable, affluent suburbs on the outskirts of cities are Type A. Blue: Still desirable neighborhoods are Type B. Yellow: Older areas are declining, Type C. Red: Exceeding a 5% Black population, the riskiest and undesirable neighborhoods are Type D.